Grupa Kapitałowa Grupa Azoty

Choose a company

The consolidated net profit for the period was nearly PLN 356m, whereas a year earlier it came in at PLN 458m. The results were weaker than in H1 2015, with EBIT down by nearly PLN 96m, EBITDA by PLN 82m, and revenue by PLN 476m. The EBIT and EBITDA margins in H1 2016 were 9.5% and 15%, respectively, a slight decrease year on year (10.5% and 15%).

EBITDA for Q2 2016 was reported at PLN 178m (against PLN 292m in Q2 2015) and net profit reached PLN 49m (versus PLN 152m), on revenue of nearly PLN 2.16bn (versus PLN 2.28bn).

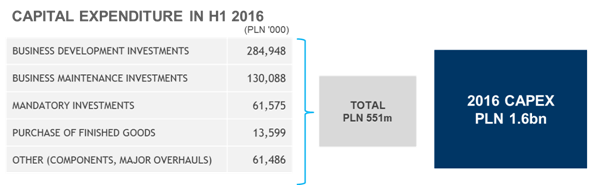

“After a very good first quarter of the year, in the second quarter our performance was affected by major shifts in the market environment, particularly in the fertilizer business. The global oversupply of fertilizers and changes in the market of key raw materials, mainly natural gas, had a major impact on the prices of ammonia and urea, which dropped by more than 30% year on year. As a result, we had to adjust our price lists, both for nitrate and compound fertilizers. Taking advantage of opportunities to diversify our product base, in the second quarter of 2016 we continued to pursue our strategies of using cheaper urea in our chemical products (mainly melamine), which to a certain extent offset the falling margins in the fertilizer segment. This helped us keep EBITDA for the Group as a whole at comparable year-on-year levels,” comments Paweł Łapiński, Vice President of Grupa Azoty, responsible for finance. “Aware of the movements in the market and limited prospects for feedstock premium, we seek to build an optimum capital expenditure portfolio. Meeting business targets and keeping financial indicators at safe levels are our priorities,” adds Paweł Łapiński.

In the Fertilizer segment, the first half of the year (first quarter in particular) is the peak season for fertilizer application and a time when distributors build stocks for autumn and production plants have maintenance shutdowns (second quarter). Accordingly, the segment’s EBIT margin moved in line with the typical trends − in Q2 2016 it fell to 5%, from 21% in Q1. In this context, it should be noted that a PLN 24.4m impairment loss on receivables and inventories was recognised in the compound fertilizer segment and the depreciation and amortisation charges rose by PLN 21m in Q2 2016, with effects to be seen in the coming quarters. Overall, in H1 2016, the segment’s EBITDA came in at nearly PLN 496m (down PLN 60m yoy), on revenue of PLN 2.74bn (down PLN 312m).

The Plastics segment was struggling against very strong price pressures from customers. The buy side’s clear domination on the market results in a fierce price competition, which leads to major declines in benzene/PA6 deltas in the European market and benzene/caprolactam deltas among Asian producers. This translated into an over 15% yoy decrease in the deltas and a negative EBITDA of almost PLN -25m, on revenue of PLN 571m (down PLN 104m year on year).

The Chemicals segment recorded a clear improvement in performance and profitability, driven primarily by continued positive margins on sales of melamine, where a sound profitability increase was seen on the back of supply fluctuations on the European market (mainly in Q1) and feedstock premium. The OXO segment also provided reasons for satisfaction. A clear increase in sales of Oxoviflex, a new flagship product, was reported, with a higher premium to propylene. In the sulfur area, global prices of liquid sulfur and prilled sulfur went down, which was reflected in Siarkopol’s lower revenue from exports. An improvement of margins in the insoluble sulfur group should also be noted; it was an effect of restructuring measures, namely the decommissioning of an inefficient carbon disulfide plant, written off in Q4 2015. On a consolidated basis, the Chemicals segment closed H1 2016 with sales of PLN 1.12bn (down approximately PLN 82m yoy) and EBITDA of PLN 165m. Thus, its profit margin was nearly 7% higher than in the corresponding period of 2015.

In Q2 2016, Grupa Azoty Puławy earned a net profit of PLN 66m (Q2 2015: PLN 95m), on revenue of PLN 809m (Q2 2015: PLN 848m). In H1 2016, net profit was reported at PLN 227m (H1 2015: PLN 269m) and revenue at nearly PLN 1,761m (H1 2015: PLN 1,919m).

Grupa Azoty Police Group’s consolidated results

With the PLN 24.4m impairment loss on receivables and inventories recognised in the compound fertilizer segment, in Q2 2016 Grupa Azoty Police earned a net profit of PLN 10m (Q2 2015: PLN 56m), on revenue of PLN 605m (Q2 2015: PLN 693m). In H1 2016, net profit adjusted for the impairment loss was PLN 78m (H1 2015: PLN 107m), on revenue of PLN 1,292m (H1 2015: PLN 1,439m).

In Q2 2016, Grupa Azoty Zakłady Azotowe Kędzierzyn earned a net profit of PLN 28m (Q2 2015: PLN 12m), on revenue of PLN 411m (Q2 2015: PLN 397m). Net profit for the first six months of 2016 was PLN 94m (H1 2015: PLN 73m), on revenue of PLN 852m (H1 2015: PLN 939m).